Many new large and complex tax laws have been passed in the last decade, with clauses slowly taking effect through time and being clarified by the IRS to this day. These include the original Tax Cuts and Jobs Act (TCJA) of 2017, the Setting Every Community Up for Retirement Enhancement (SECURE) Act of 2019, the SECURE Act 2.0 of 2022, the Inflation Reduction Act (IRA) of 2022, and the One Big Beautiful Bill Act (OBBBA) of 2025.

With these new complexities on top of the already-existing complicated tax laws, instead of waiting until the end of the year, we want to encourage everyone to get pertinent tax advice from their team of financial, legal, and tax professionals now, mid-year, while they still have plenty of time to take action.

Personalized tax advice from tax professionals is always recommended. But we wanted to give you a few things to consider, for informational purposes only.

Can I benefit from charitable contributions?

- For non-itemizers, you can still claim an “above the line” deduction on your 2026 tax return for cash gifts to qualifying charities, excluding donor-advised funds and private foundations. Single people can claim up to $1,000; married up to $2,000. NOTE: Non-cash or in-kind donations of property are not deductible for those using the standard deduction.

- For those who itemize, you can still use Schedule A, but you can only deduct contributions that exceed .5% of your adjusted gross income. For example, if your AGI is $100,000, only donation amounts in excess of the first $500 are tax-deductible. Non-cash, in-kind donations are deductible over the threshold, but must meet new, stricter rules to substantiate fair market value of the items. For donated items valued over $500, you must file IRS Form 8283, and an independent appraisal is generally required for property valued over $5,000. For those in the top income tax bracket (37%), the tax benefit of charitable deductions is reduced from 37 cents to 35 cents per dollar donated.

- If you have a tax-deferred IRA (individual retirement account) and you are at least 70-1/2 years old, you might be able to make a direct QCD, or Qualified Charitable Contribution to an eligible nonprofit, allowing you to exclude up to $111,000 from your gross income. You can also use QCDs to satisfy your annual required minimum distributions, eliminating part or all of your tax bill on otherwise taxable RMDs.

Can I “bunch” my tax deductions?

With the standard deduction amount at $16,100 for single filers and $32,200 for those filing jointly in 2026, itemizing your tax returns only makes sense if your deductions exceed these amounts. Bunching multiple years’ worth of charitable donations, state and local taxes (SALT), large medical expenses, and other claimable deductions into a single tax year may be possible to help you surmount the standard deduction threshold.

Will I be able to make catch-up contributions for the 2026 tax year?

Maximizing contributions to tax-deferred qualified accounts is a strategy used by some to reduce taxable income. For those aged 50 or older, be aware that there are new requirements for catch-up contributions to workplace plans for 2026.

- $150,000 or less in income

For those who earn less than $150,000, you can still make catch-up contributions to your workplace traditional 401(k) or similar pre-tax accounts, or to your Roth accounts if your employer offers them. It’s your choice. Those aged 50 or older can contribute an additional $8,000 catch-up amount on top of their standard $24,500 contribution limit for 2026, while those aged 60 through 63 are allowed “super catch-up” amounts of $11,250.

- $150,000 income or more

For those who earn $150,000 or more, catch-up contribution amounts can only be made to after-tax Roth accounts beginning this year. If your workplace doesn’t offer a Roth option, you cannot make catch-up contributions in 2026.

- IRA catch-up amounts

For those who own their own traditional IRA or Roth IRA accounts, you may be able to contribute $7,500 for 2026 if you meet income and other IRS requirements. If you are 50 or older, an additional $1,100 catch-up amount may be allowed.

Do I have more tax write-off options as a sole-proprietor or business owner?

The short answer is yes. Here are a couple of recent tax laws that may apply to you as a business owner, but there are many more tax opportunities for businesses you may want to explore.

The OBBBA permanently provides immediate 100% bonus depreciation for eligible assets like vehicles or equipment allowing businesses to write off the entire cost of qualifying property upfront. Bonus depreciation can also be used to create or increase a net operating loss which can be carried forward to offset future taxable income.

The OBBBA also made the QBI deduction permanent with expanded access to more businesses. Pass-through businesses (meaning profits pass through your business to your personal tax return) may be eligible to deduct up to 20% of their QBI or qualified business income if they meet eligibility requirements.

Can a series of Roth conversions help my tax situation?

For those heading toward retirement, don’t forget to explore long-term tax strategies like Roth conversions that you might be able to utilize. There are two ways Roth conversions can reduce taxes for some people. First, you might be able to reduce your overall income tax burden in retirement. Second, you might be able to reduce taxes for your heirs, transferring more wealth to the next generation.

- For You

Most qualified retirement accounts like 401(k)s are funded with pre-tax dollars. Meaning that your employer diverts your selected contribution amount into your 401(k) account, reducing your annual taxable income by the amount you have contributed. Traditional IRAs (individual retirement accounts) are also funded with pre-tax dollars, and some taxpayers can take tax deductions for IRA contributions if they qualify.

Pre-tax contributions can reduce your taxes while you are building up retirement assets. However, as you get close to retirement, you need to remember that ordinary income taxes will be due on all of that money, and you will be required to start annual withdrawals at age 73, paying income taxes on those amounts every year. Plan custodians are not required to inform you about these RMDs (required minimum distributions), or calculate them for you. You must proactively take them. And there’s no grace period either, RMDs are due by December 31 at midnight each year, not April 15 tax day, with exceptions only in your first year of taking RMDs.

And, surprise! Many find that RMDs from large taxable accounts cause their Social Security benefits to be taxed—from 50 to 85% in some cases when their annual “provisional income” exceeds $44,000 for married couples filing jointly; $25,000 for single filers.

Roth conversions allow you to move money from taxable accounts like traditional 401(k)s over to after-tax Roth IRA accounts, depending on your plan’s rules. If these are done after age 59-1/2, no penalties will apply, but you will owe income taxes on amounts converted in the tax years you make conversions. So, keep in mind this tax strategy only makes sense if you will benefit over the long-term.

Be sure to find professionals you trust to do the math for you and follow all strict IRS rules as Roth conversions cannot be undone. And be sure to ask your financial professional if there are ways to pay for the income taxes that will be due.

As a reminder about Roth accounts, RMDs are not required from them, and any withdrawals you do decide to make are not subject to income tax since they are funded with after-tax money. Principal you have put in can be taken out of a Roth at any age without tax consequences, and same with earnings after five years after you reach age 59-1/2. (Hardship rules apply if you really need to access funds.)

- For Your Heirs

Many people still don’t understand that non-spousal inheritance rules for traditional taxable accounts like 401(k)s changed drastically because of the SECURE Act of 2019, requiring that the entire inherited account balance be fully withdrawn by the end of the 10th year following the original owner’s death. This change can cause heirs to be thrown into the highest income tax brackets, eating away a large chunk of their inheritance due to taxes. Furthermore, annual RMDs have to be taken by inheritors based on their own life expectancies if the original owner had been taking RMDs. (Note: there are exceptions for Eligible Designated Beneficiaries (EDBs).)

According to the Congressional Research Service, this change, which took effect in 2020, will generate $15.7 billion+ of additional federal tax revenue through 2030; the huge bump coming from compressing these distributions into a single decade.

If you have large taxable accounts and had hoped to leave tax-advantaged legacy wealth to your heirs, be sure to look into how Roth conversions might impact your estate plan in terms of passing on multigenerational wealth. Roth IRAs can be left to heirs tax-free after the account has been in place for five years or more. The only new rule is that heirs must withdraw and close a Roth account within 10 years of inheritance.

###

How will I be able to retire?

If you are concerned about how you will be able to afford to retire, how and when you might finally be able to quit your job, and how you can build tax advantages into your retirement plan, don’t hesitate to reach out to us for a complimentary conversation. Remember that having a 401(k) plan or a portfolio of stocks and bonds is not the same as having an actual retirement plan that maps out your monthly income during the 20, 30, or even 40+ years you might live in retirement.

We focus on retirement planning. You can reach The Financial Education Group by calling (360) 900-3837 or setting up an appointment with us here.

This content is for informational and educational purposes only and should not be construed as tax, legal, or individualized financial advice. Always consult with your tax advisor, attorney, and/or qualified financial professional regarding your specific situation before making any retirement plan or tax-related decisions. Retirement plan provisions can vary based on plan design, employer implementation, and individual circumstances. Roth availability and catch-up contribution rules are subject to plan amendments and IRS guidance.

Sources:

https://www.schwab.com/learn/story/social-security-is-taxable-how-to-minimize-taxes

https://www.fidelity.com/learning-center/personal-finance/tax-brackets

https://www.irs.gov/taxtopics/tc506

https://www.landmarkcpas.com/qbi-deduction-2026-changes-what-business-owners-need-to-know/

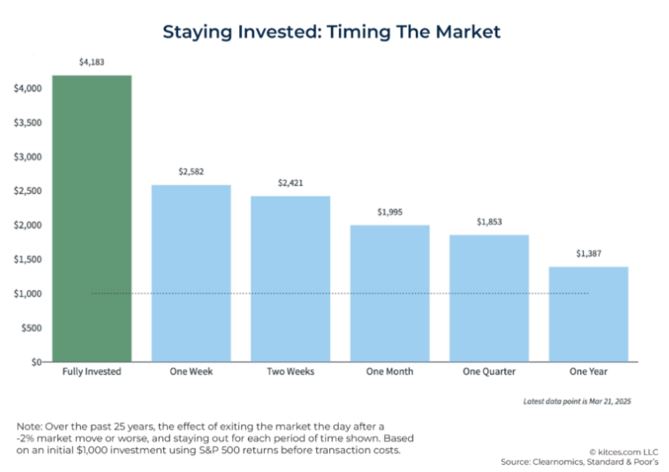

This chart shows that those who exit the market the day after every -2% market move or worse over a 25-year time period usually underperform those who remain fully invested. When you leave the market, you don’t just avoid future bad days, you also miss out on the future good days. Ultimately, missing even just a few of the market’s best days, or getting back into the market only after the market is already up, can significantly impact long-term returns. Because, remember, just like in life, nothing stays bad forever; good days will come again. The market is no different.

This chart shows that those who exit the market the day after every -2% market move or worse over a 25-year time period usually underperform those who remain fully invested. When you leave the market, you don’t just avoid future bad days, you also miss out on the future good days. Ultimately, missing even just a few of the market’s best days, or getting back into the market only after the market is already up, can significantly impact long-term returns. Because, remember, just like in life, nothing stays bad forever; good days will come again. The market is no different.